Learn about Property Costs and our essential tips to prepare you for all the upfront and continues expenses of buying a house in South Africa.

Buying a property is an exciting and monumental step for any individual, often regarded as one of the most significant financial commitments you’ll make in your lifetime. Whether you’re a first-time buyer or someone with prior experience, setting a realistic budget and aligning it with your expectations is crucial step that many buyers don’t thoroughly consider prior to diving into the property market.

Not only that, but you also need to take a comprehensive look at your financial health. This goes beyond assessing what you can afford today, it includes understanding your long-term commitments and creating a budget that allows you to thrive, not just survive, in your new home.

Table of Contents

Join us as we cover some of the essentials of budgeting, saving for upfront costs, and conducting market research to ensure you’re fully prepared for this exciting venture.

Breaking Down the Costs

When purchasing a property, the total cost extends well beyond the sale price. Understanding these costs ensures you don’t encounter unpleasant surprises.

Monthly Bond Repayments

Your bond (or mortgage) repayment will likely be your largest monthly expense. In South Africa, home loans typically span 20 years, though shorter and longer terms are available.

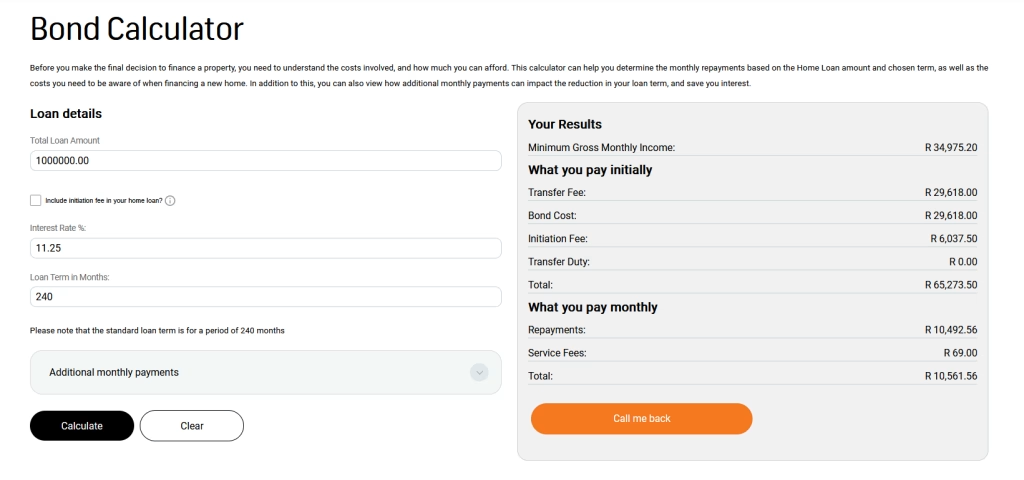

The current repo rate in South Africa is 7.75%, and the corresponding prime lending rate is 11.25%, as of January 2025. These rates reflect the latest adjustments by the South African Reserve Bank (SARB), which reduced the repo rate by another 25 basis points since the previous rate of 11.5% at the end of 2024. On the upside, there are talks of further reductions during the course of the year, which is only a positive for current and potential homeowners.

Using these rates, the bond repayment on a loan of R1 000 000 over a typical 20-year term would be calculated as follows:

- Monthly Bond Repayment:

- At an interest rate of 11.25%, the repayment is approximately R10,492 per month.

- Total Cost Over 20 Years:

- Estimated total repayments would amount to R 2,518,214

To be approved for a R1,000,000 bond, your required minimum Gross Monthly Income should be roughly: R34,975.00. To get a detailed breakdown of Min required Gross, Transfer Fee’s, Bond cost, monthly bond repayments you an check out: FNB Bond Calculator

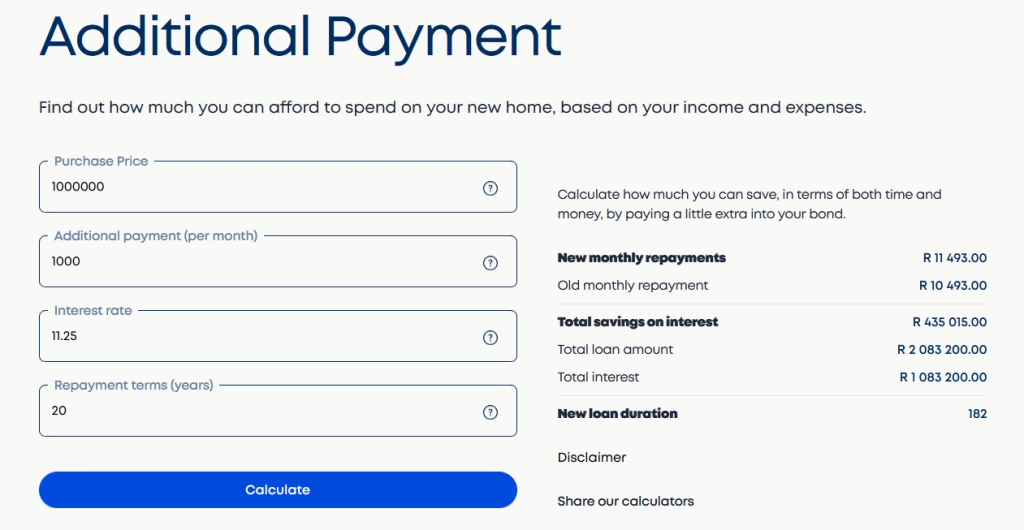

Accelerating Your Bond Repayment

Making additional monthly payments can significantly reduce the total interest paid and the term of your bond:

- Adding R500/month:

- Reduces the bond term by almost 3 years.

- Saves approximately R 260,749 in interest.

- Adding R1,000/month:

- Shortens the bond term by almost 5 years.

- Saves over R435,000 in interest.

Use online tools like the BetterBond Additional Payment Calculator to test scenarios based on your financial goals.

Anticipated Future Rate Cuts

SARB’s monetary policy committee has indicated the potential for further rate reductions in 2025, depending on inflation trends and economic conditions. Analysts suggest the repo rate could drop closer to 7%, which would decrease monthly repayments further. For example, if the prime rate were reduced to 11%, the repayment on a R1,000,000 bond would fall to approximately R10,390/month, offering additional savings to borrowers.

Recommendations

- Make Extra Payments Early: Reducing your loan principal sooner yields compounding savings, particularly if rates drop.

- Monitor SARB Announcements: Stay informed about rate changes by following updates from the South African Reserve Bank.

- Consider Refinancing: If rates drop substantially, refinancing at a lower rate may reduce your repayment burden.

- How They Are Calculated:

Bond repayments depend on three factors: the loan amount, the interest rate, and the loan term. For example, borrowing R1,000,000 at an interest rate of 10% over 20 years will cost approximately R9,650 per month. - Practical Tip:

Use bond calculators on platforms like BetterBond or Property24 to estimate your monthly repayments. Include a buffer for potential interest rate hikes.

Rates, Taxes, and Levies

Owning a property comes with ongoing costs like municipal rates, taxes, and—if you buy a sectional title property—monthly levies.

- Municipal Rates and Taxes:

These are calculated based on the municipal value of your property. The rates are used to fund services like waste collection and road maintenance. Contact your local municipality to understand the rates in your desired area. - Levies for Sectional Titles:

For townhouses or apartments, levies cover shared expenses like security, maintenance, and communal amenities. Always request a breakdown of levies before committing to a sectional title property.

Home Insurance and Maintenance

- Insurance: Lenders often require you to take out home insurance, protecting your property against unforeseen damage.

- Maintenance Costs: Create a savings plan for repairs. Freehold homeowners should budget approximately 1% of the property’s value annually for maintenance.

Renovations and Upgrades

- Renovation and Upgrades: These costs can vary widely depending on the scope of the work, the age of the property, and the materials used. To avoid financial strain, it’s important to budget and plan for these potential expenses upfront and also factor it into your purchase price. You do not want to get yourself into a situation where you overcapitalize on your property. If you’re not a contractor or builder, it is best to get professional advise and do a thorough property inspection upfront to ensure you know what you are getting yourself into.

Saving for Upfront Property Costs

Many buyers focus on monthly repayments but underestimate the importance of upfront property costs. Saving for these expenses is a critical step in your home-buying journey.

The Deposit

While some banks offer 100% bonds, providing a 10% to 20% deposit of the purchase price can significantly reduce your loan amount, lower your monthly repayments, and improve your chances of securing a favorable interest rate.

- Setting a Savings Target:

For a R1,000,000 home, aim for a deposit of R100,000 to R200,000. - Practical Saving Tips:

Bond Registration

This is a one-time fee paid to the bank-appointed attorney responsible for registering the bond in your name. The fee varies depending on the size of the loan, and it is typically calculated according to the Law Society’s tariffs. The process involves legal steps to ensure that the bond is properly recorded and that the bank’s interest in the property is secured.

Transfer Costs

This is another one-time fee, but it is paid to the conveyancing attorney who handles the transfer of ownership of the property from the previous owner to you. These costs are typically based on the purchase price of the property and include all the necessary legal steps to finalize the ownership transfer.

Transfer Duties

Transfer duties are a tax paid to the South African Revenue Service (SARS) when purchasing a property valued over R1 million. The amount of transfer duty depends on the property’s purchase price and follows a progressive scale. This is separate from VAT and is due at the time of transfer to ensure the buyer’s legal claim to the property.

- Pro Tip: First-time buyers purchasing properties below R1 million are exempt from transfer duty, making this price point a strategic entry into the market. Furthermore, you can and should negotiate your Bond and transfer cost and ask for a reduction from the attorney during the initial stages. In some instances certain attorneys will offer you lower rates if you request to use them for both Registration and Transfer.

To get a rough estimate on cost there are numerous online calculators available, for example: BetterBond Bond and Transfer Calculator

Conducting Market Research

Market research is your compass in the property-buying process and should be key to your decision making. By analyzing trends, property values, and growth potential, you can ensure your investment aligns with your financial goals and lifestyle.

Understanding Property Values

Property prices in South Africa vary significantly between provinces, cities, and even neighborhoods. Researching values in your target area gives you an edge in negotiations.

- How to Compare Prices:

Use platforms like Private Property and Property24 to compare listing prices, rates and levies in the different areas. - Historical Trends:

Tools like Lightstone Property can provide data on the growth trajectory of specific areas, last sales price of the property, average sales prices of properties in the area and numerous other info.

Evaluating Growth Potential

The value of your property investment depends not only on its current state but also on its future prospects.

- Urban Growth Hotspots:

Look for areas with expanding infrastructure, such as new schools, business hubs, or public transport links. - Examples of Growth Areas:

- Johannesburg: Suburbs like Fourways and Midrand are seeing rapid development.

- Cape Town: The Northern Suburbs are popular among young professionals.

- Durban: Coastal towns along the North Coast are becoming lifestyle investment hubs.

Buyer’s Market vs. Seller’s Market

- Buyer’s Market: Prices are lower due to oversupply. This is ideal for securing bargains.

- Seller’s Market: Demand outstrips supply, often leading to competitive bidding. Be cautious about overpaying in this scenario.

For more details, check out our post: Buying Property? The Property Market & Market Trends You Need to Know

Staying Informed

- Subscribe to newsletters from real estate firms like Pam Golding or RE/MAX.

- Follow economic updates from Moneyweb to gauge market conditions.

Setting Realistic Expectations

Balancing your wish list with what’s feasible is essential for a successful property purchase.

Assessing Needs vs. Wants

- Must-Haves: Determine non-negotiables, such as proximity to schools, safety, or the number of bedrooms, bathrooms, garages etc.

- Nice-to-Haves: Features like a swimming pool or a large garden can be deprioritized if they don’t fit your budget.

Urban vs. Suburban Living

Consider whether you prioritize space and tranquility (suburbs) or convenience and proximity to work (urban areas). Each has distinct cost implications for example monthly fuel usage for driving to work, schools etc.

Key Takeaways

- Budget Wisely: Start with a clear understanding of your monthly expenses and affordability limits. Use tools like bond calculators to model different scenarios.

- Save Strategically: Focus on building a deposit and covering upfront costs like legal fees, transfer duties, and bond registration.

- Research Thoroughly: Analyze property values, market trends, and growth potential to identify the best areas for investment.

- Align Expectations: Be realistic about your financial capacity and prioritize essentials over luxuries.

By establishing a solid financial foundation and conducting detailed research, you can confidently take the first steps toward property ownership. This preparation not only ensures a smooth buying process but also positions you for long-term success in managing your investment, where it becomes an asset not a burden.

Join the Conversation: Got comments, questions, or want me to write about something specific? Drop them in the comments section below.